How Should Wire Drawing Die Manufacturers Cope with the Resource Shortage?

The Tungsten Market Stalemate in 2026: Beneath the Calm Surface, How Should Wire Drawing Die Manufacturers Cope with the Resource Shortage?

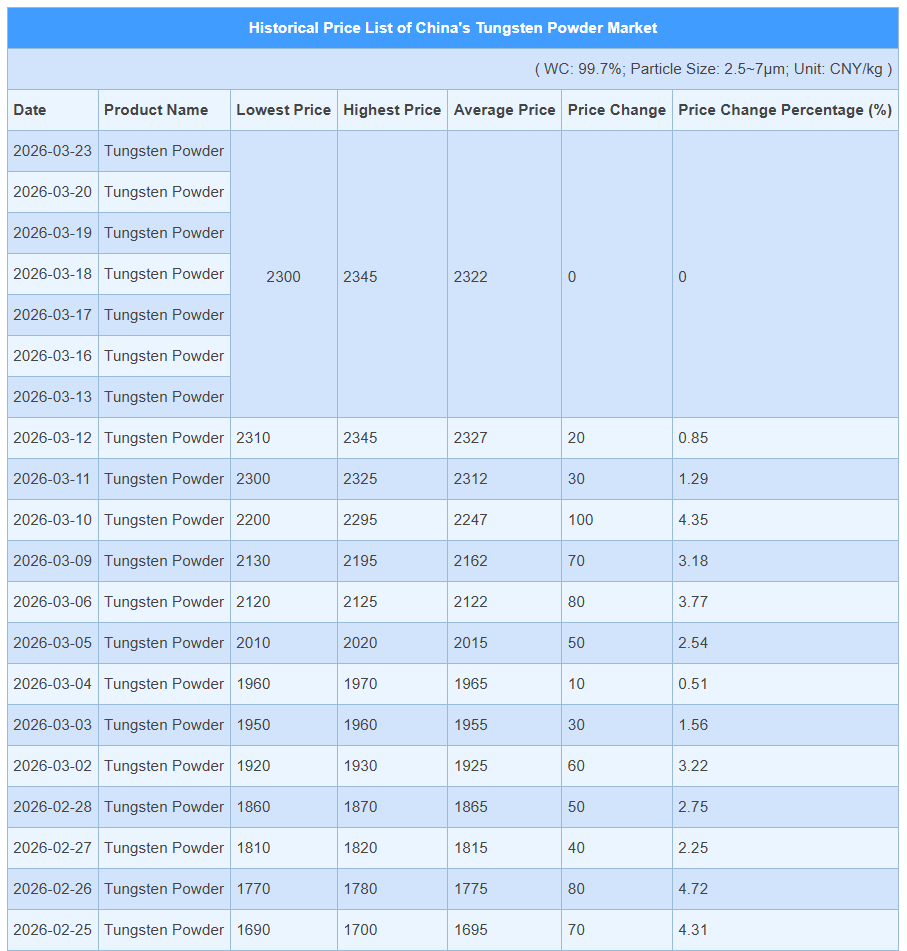

Beneath the market’s surface calm lies a strategic standoff as buyers and sellers enter a phase of rational wait-and-see. Faced with raw material costs exceeding one million yuan per ton, downstream processing enterprises have become extremely cautious in their procurement, focusing primarily on essential needs. Meanwhile, mines and traders holding resources are in no hurry to sell after experiencing rapid price hikes earlier. This stalemate has temporarily stabilized prices at high levels.

In contrast to the “stability” of China’s domestic market, the international market remains robust. European APT quotes range from $1,890 to $1,998 per metric ton, which, when converted to RMB, remains higher than domestic prices. This divergence between domestic and international markets stems from China’s strict controls on tungsten mining and exports. China supplies over 80% of the world’s tungsten; when supply tightens at the source, the reaction in overseas markets is often more severe.

The contraction on the supply side is inevitable. In 2026, China’s total tungsten ore mining quota was reduced once again. This is not a spur-of-the-moment decision but a continuation of China’s policy of protective mining for strategic resources. At the same time, the normalization of environmental and safety regulations has made production unstable for many small and medium-sized mines, forcing some to exit the market and passively increasing industry concentration.

The gradual depletion of high-grade tungsten ore reserves is another inescapable reality. Mining costs continue to rise, while the lengthy commissioning cycles of new overseas mining projects mean that distant solutions cannot address immediate needs. Analysts at China’s Shanghai SteelHome point out that the situation of rigid supply-side contraction will not change in 2026. This implies that the total volume of tungsten that can be extracted from mines has been firmly capped.

When the supply ceiling is lowered, even the slightest growth on the demand side is magnified. Traditional sectors, such as cemented carbide cutting tools and specialty steels, have consistently stable demand and form the core of tungsten consumption. The real variables come from emerging sectors.

Photovoltaic tungsten wire is currently the strongest driver of demand. As N-type silicon wafers trend toward thinner profiles, the strength requirements for cutting wires are becoming increasingly stringent. Thanks to their high strength and wear resistance, tungsten diamond wires have achieved a market penetration rate exceeding 80%. Behind every high-efficiency photovoltaic panel lies the indispensable role of these ultra-fine tungsten wires. Some institutions predict that by 2026, demand growth for photovoltaic tungsten wires alone could exceed 90%.

The surge in semiconductors and artificial intelligence has driven up demand for high-end products such as high-purity tungsten targets and tungsten alloys used in chip packaging. Additionally, in the aerospace and defense sectors, tungsten serves as the core material for critical components like armor-piercing projectiles and rocket nozzles, leading to increased strategic reserves and actual consumption. These high-end applications not only involve large volumes but are also price-insensitive, further solidifying the foundation of tungsten prices.

Inventories across the entire industry chain are at historic lows. Following sustained price increases and downstream consumption, raw material stocks are low at every stage—from mines to smelters to processing enterprises. Spot supplies in the market have become scarce, giving holders stronger bargaining power. Some powder metallurgy companies have already issued price increase notices due to cost pressures, while some small and medium-sized enterprises facing tight cash flows have even begun suspending new orders.

The sharp price surge is reshaping the profit landscape across the entire tungsten industry chain. Upstream companies with their own mines are undoubtedly the biggest beneficiaries. The stock prices of leading companies such as China Zhangyuan Tungsten and Xiamen Tungsten have doubled or more since 2026. Profits are flooding toward the resource end of the chain.

The midstream smelting and processing segments, however, are caught between a rock and a hard place. Raw material costs remain sky-high, yet passing these costs entirely on to downstream buyers faces resistance. This is forcing midstream enterprises to upgrade their product portfolios, shifting production capacity toward high-value-added products such as photovoltaic tungsten filaments and high-purity tungsten materials.

For downstream hardmetal tool manufacturers, this cost crisis has become a brutal survival of the fittest. Companies that rely solely on purchasing tungsten powder and tungsten carbide powder for low-end processing have seen their profit margins severely squeezed, making survival difficult. In contrast, companies with core technologies capable of producing high-end CNC cutting inserts and modular tooling products can absorb some of the costs through technology premiums and even gain a larger market share.

An overlooked sector is now seeing opportunities emerge: tungsten recycling. When the supply of primary tungsten ore is tight and prices are high, recovering tungsten from scrap cemented carbide and grinding waste becomes a lucrative business. At the policy level, there is also encouragement for the development of “urban mines” and the improvement of the recycling system for renewable resources. Companies with the technology to efficiently extract tungsten from low-grade tailings and complex waste materials are becoming new value nodes in the industrial chain.

Against this backdrop, what path should wire drawing die manufacturers—major consumers of tungsten—take?

Soaring raw material prices have directly driven up the manufacturing costs of wire drawing dies. Many manufacturers face immense cost pressures, with some even seeing their profit margins severely squeezed. To address this challenge, wire drawing die manufacturers must actively seek solutions.

First, companies can strengthen raw material procurement management, establish stable supply channels, and explore avenues for recycling waste tungsten to reduce raw material costs. Second, companies can leverage technological innovation to develop higher-performance, more competitive wire drawing die products, using technology premiums to offset some of the costs. Additionally, companies can reduce production costs and enhance competitiveness by improving production efficiency and optimizing management processes.

The trend in tungsten prices has transcended the cyclical fluctuations typical of ordinary commodities. It is driven by the dual logic of “resource national security” and “industrial upgrading needs.” When a material is simultaneously critical to high-end manufacturing, new energy, and national defense security, the factors supporting its price become exceptionally complex and robust.

Market participants are now concerned about how long this high-level stabilization will last. In the short term, the tight supply-demand balance is unlikely to be disrupted. The global tungsten market may face a supply shortfall of over 20,000 metric tons by 2026. Low inventory levels across the supply chain also make prices exceptionally sensitive to any disruptions on the supply side.

#WireDrawingDies #Tungsten #Costs #Challenges #Countermeasures