Deep Analysis of the Supply-Demand Dynamics Behind Tungsten

Prices Hitting All-Time Highs

| Product Name | Price | Change | Unit | Date |

|---|---|---|---|---|

| Tungsten Concentrate | 82.4 | +15000 | CNY/ton | 2026/03/02 |

| APT | 119 | +25000 | CNY/ton | 2026/03/02 |

| Tungsten Powder | 1925 | +50 | CNY/kg | 2026/03/02 |

| Tungsten Carbide | 1865 | +50 | CNY/kg | 2026/03/02 |

| Scrap Tungsten Grinding Material | 13.45 | +0.3 | CNY/kWh | 2026/03/02 |

| Ferro-Tungsten | 1,105,000 | +10000 | CNY/ton | 2026/03/02 |

| Cobalt Powder | 580 | 0 | CNY/kg | 2026/03/02 |

I. Current Price Status and Historical Comparison

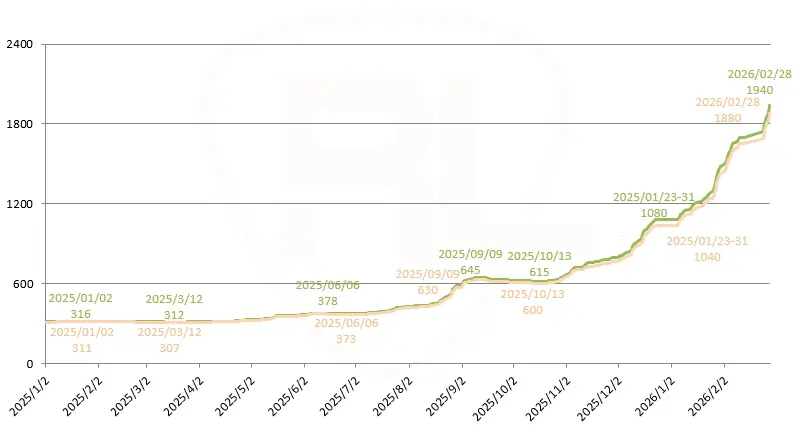

As of February 2026, black tungsten concentrate (65% WO₃) reached 745,000 CNY/ton, ammonium paratungstate (APT) exceeded 1 million CNY/ton, and tungsten powder surpassed 1,800 CNY/kg—all setting historical records. Compared to early 2025 levels of around 143,000 CNY/ton for black tungsten concentrate, this represents a full-year increase of 343%. Relative to March 2024’s 130,000 CNY/ton, the two-year cumulative rise exceeds 240%.

Latest spot data shows black tungsten concentrate breaking through 800,000 CNY/ton, APT reaching 1.2 million CNY/ton, and tungsten powder at 1.94 million CNY/ton, with single-day gains around 2%. These figures align with real-time market reports from sources like Mysteel and Chinatungsten Online, confirming the ongoing surge into early March 2026.

**Tip: Price trend chart of tungsten powder and tungsten carbide powder, January-February 2026

Unit: CNY/kg Green line: Tungsten powder Yellow line: Tungsten carbide

II. Persistent Tightening on the Supply Side

China dominates global tungsten supply (approximately 85%), but production quotas have declined year by year: down 6.45% in 2025 and another 8% in 2026. Environmental enforcement in regions like Jiangxi has led to mine closures, keeping industry operating rates chronically below 60%.

Resource depletion adds pressure: national tungsten ore grades fell from 0.42% in 2004 to 0.28% by 2016, with high-grade deposits becoming increasingly scarce. The first batch of 2025 mining quotas was only 58,000 tons, a reduction of 4,000 tons year-over-year. Tungsten is classified as a dual-use item under export controls, strengthening China’s pricing power and resulting in overseas prices carrying a 20-30% premium over domestic levels.

III. Explosive Growth on the Demand Side

Photovoltaic Revolution: Tungsten wire has replaced diamond wire for silicon wafer cutting, with penetration jumping from 20% to 60%. Tungsten consumption per GW of silicon wafers rose from 2 tons to 8 tons, driving global photovoltaic demand over 4,500 tons in 2025.

Military and Aerospace: U.S. missile defense systems alone require up to 9,000 tons per project, with global military orders surging 42%. Tungsten remains irreplaceable in armor-piercing projectiles and similar applications.

Emerging Technologies: Nuclear fusion reactors (e.g., ARIES-ST designs needing 29,034 tons of tungsten) and AI server PCB micro-drills are creating new demand surges.

#TungstenCarbidePriceTrend